Will Inflation Drag On?

Will Inflation Drag On?

Slay the inflation dragon with commodity and managed futures funds.

Overview

The FOMC showed its data dependence, raising rates by 75 basis points (after previously signaling a 50-bp increase), after last week’s hot inflation and consumer sentiment readings.

The Fed acknowledged that many factors outside its control are driving inflation. As we analyzed recently, rates will have to remain higher, longer. A cartoon from the Economist magazine of the Fed dragged by the inflation dragon sums up the FOMC dilemma.

We are all data-dependent now, with the Fed on track to raise rates through the end of the year. The FOMC is looking for a “series” of flat-to-down readings before slowing rate increases, which I interpret to mean 4~6 months of data. We also expect the data dependence to add volatility to markets through September.

The S&P-500 made new lows this week, which could start another downtrend.

Commodity and managed futures funds have offered refuge in this inflation storm, and they are worth a look.

Key Question

How can the average investor take advantage of trends in the global commodity markets? For example, we pointed to the energy ETFs early this year. This week we review commodity and managed futures funds.

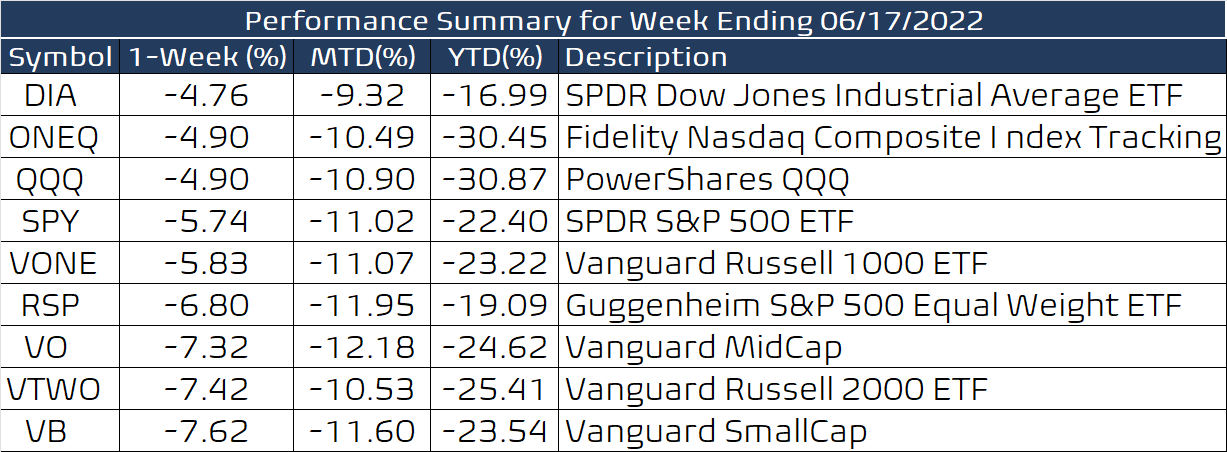

Performance Summary

A dire week in the market for stocks and bonds. The FOMC confused traders, who can now project their worst fears onto the stock market with each new economic report. As I have said for many weeks, we have to wait till the August data dump is available to get a better reading on inflation, but that means there is little reason for bulls to do anything. The downside risk is hostage to FOMC actions and traders’ fears, and one can project support near 3400, then down at 3200, and eventually 3000 on the S&P-500. The typical bear market projection (which may not mean anything here) suggests a worst-case to 3000 and a bottom by year-end.

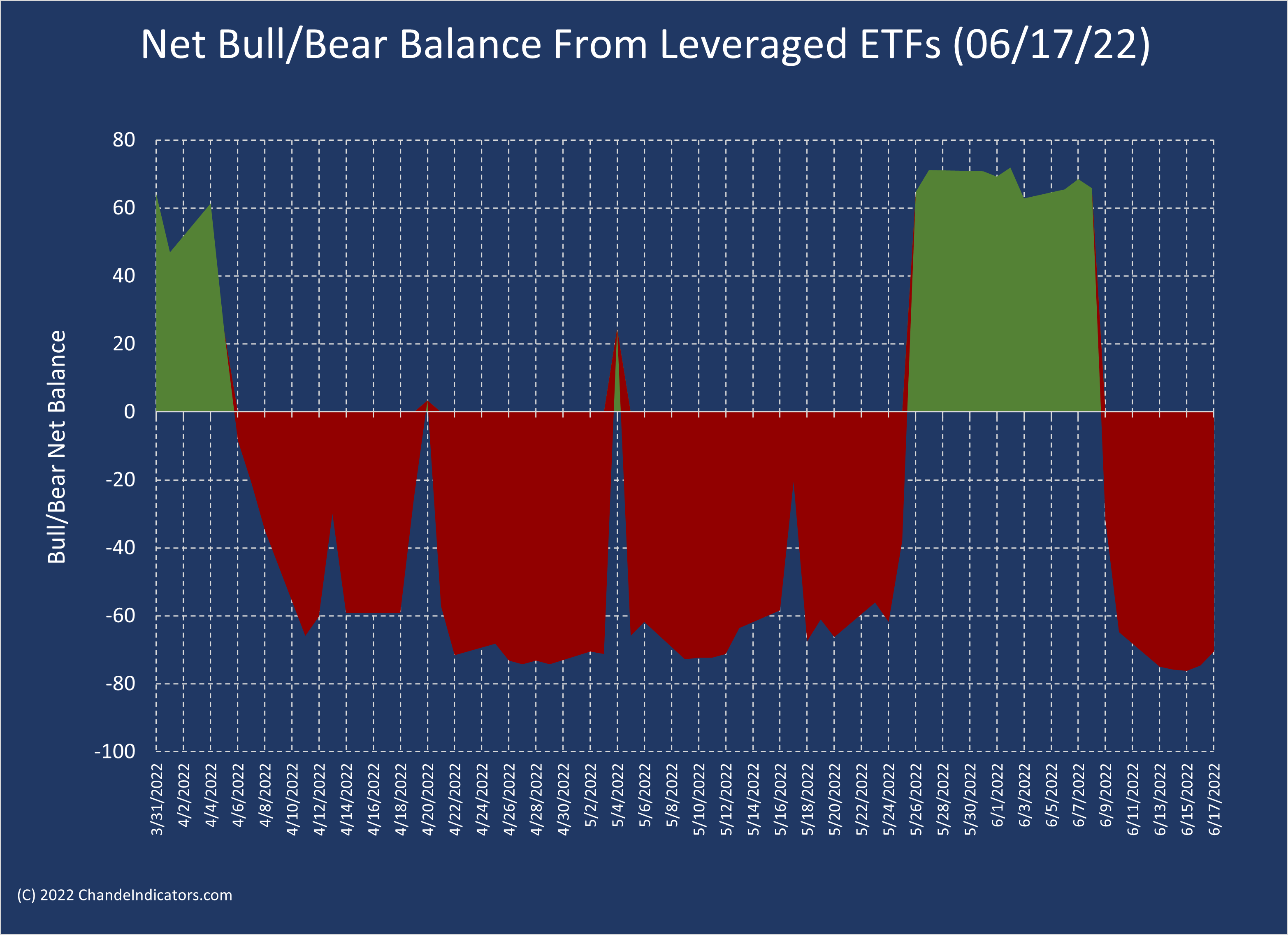

The net bull/bear balance, which has been a good barometer, is now below -70, suggesting the bearish trends will continue.

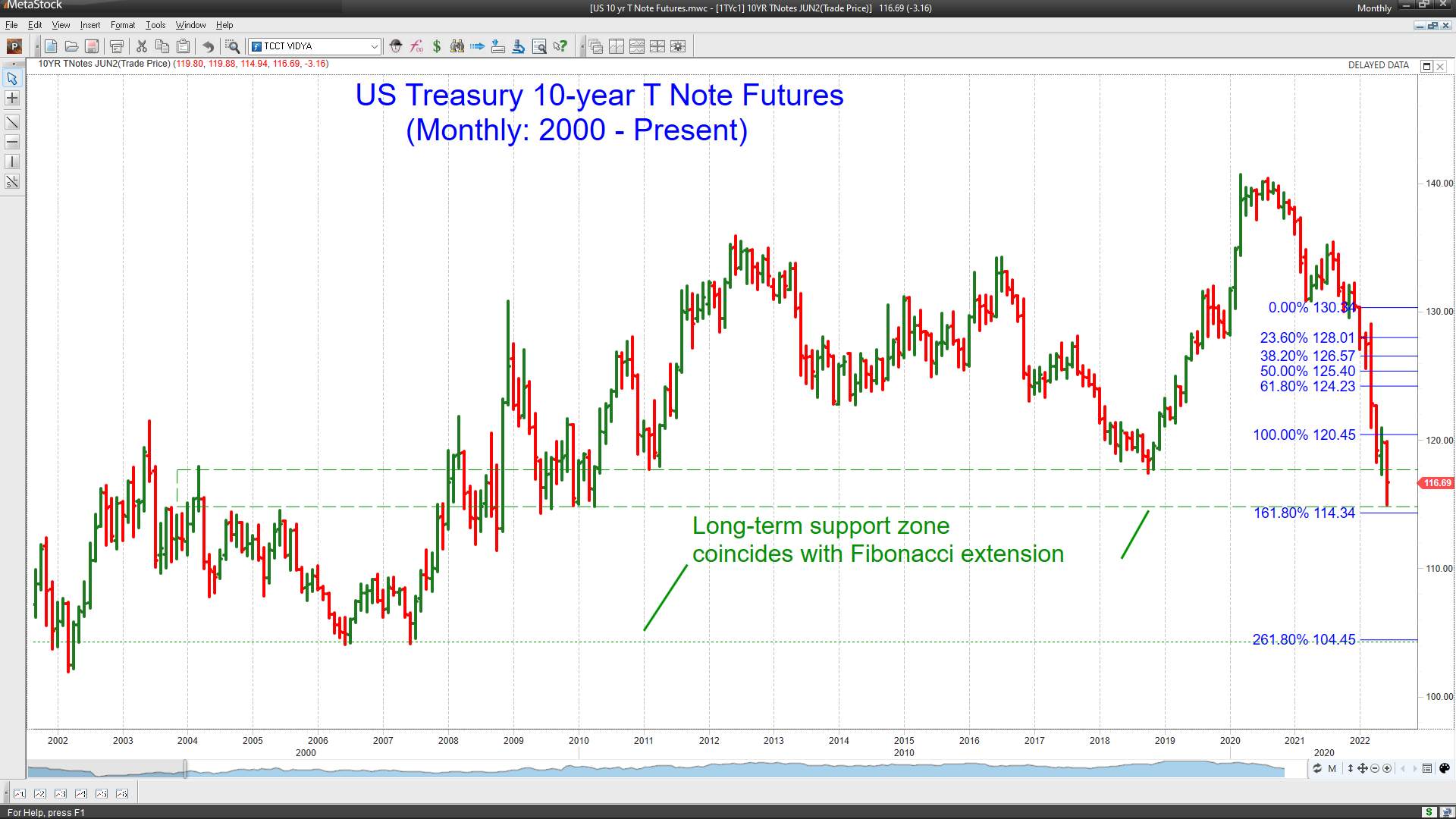

This week’s breakdown in the US 10-year note is critical, though it is still near long-term support. Any further weakness will feed directly into the stock indexes.

Commodity and Managed Futures Funds

A period of high inflation is the most favorable market environment for commodity and managed futures funds. For example, the Energy Select Sector ETF (XLE) we highlighted in January is a commodity fund, as are funds like UGA and USO (see below).

The KFA Mount Lucas Index Strategy ETF (KMLM) is an excellent example of a managed futures ETF. This ETF provides exposure to a trend-following futures-based trading strategy so that we can exploit both rising and falling prices.

These funds tend to report their data monthly, so as of May 31, the KMLM fund was up 33.49% over the previous six months. It is long grain and energy futures, short currency futures (i.e., long the US dollar), and short bond futures (which fall with rising rates). So their positioning is aligned with major market trends.

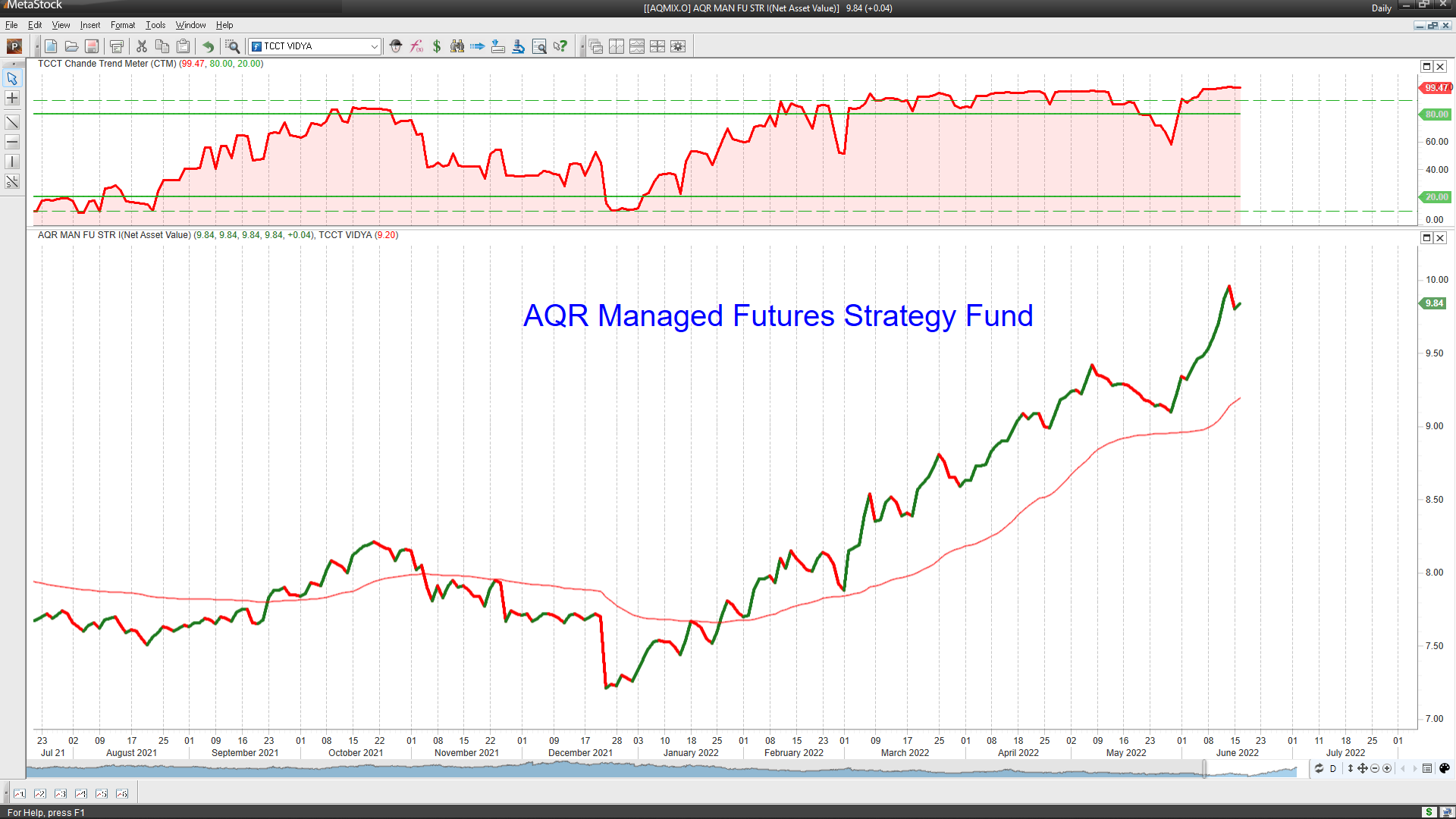

The AQR managed futures strategy fund has also performed well in the current environment. Their fund also offers exposure to commodities, currencies, and fixed income. Fortunately, persistent trends due to rising rates and higher inflation are the most potent drivers for their returns.

Note that the risk profile of such commodity funds and managed futures funds may not be suitable for everybody.

You can follow this list of symbols: FMF, DBMFB, COMT, UGA, USO, AQMIX, SOUB, WEAT, RINF, GSP, and UUP. They will give you a feel for inflationary pressures and opportunities.

Wrap-up

My posts should give you a good starting point, with context and suggestions if you like to research. Then, you can visit my website, chandeindicators.com, for more information and ideas. I hope you stay tuned and help by subscribing and recommending it to your friends and colleagues.

Thank you for spending some time with me.

Disclaimer

And now for some housekeeping. This publication is for “edutainment,” education, and entertainment, not for investment advice. Past performance is not necessarily indicative of future results. Our disclaimer at chandeindicators.com is included herein by reference.