Is a 10% Decline Imminent?

We explore if the market is poised for a decline in September.

Overview

Market sentiment soured after seeing the images of chaos in Kabul.

A brief sell-off was met with buying near the 50-day simple moving average.

Small stocks re-tested their recent lows after another bout of selling.

Key mega-cap tech stocks broke to new highs at the end of the week.

Defensive sectors continue to hold up well.

Key Question

The chaos in Afghanistan drew the market’s attention to the negatives of the current situation, namely rising COVID-19 cases, the uncertainty about the Federal Reserve’s future bond purchases, and a crackdown on technology companies in China. Can these come together to produce the 10% decline many have been forecasting for months?

Performance Summary

The market had a losing week, enduring a quick drop Monday through Wednesday, only to bounce back on Thursday and Friday. Small stocks (VTWO, VB, VO) were weak again, and large-cap tech stocks (QQQ, ONEQ) were stronger at the week’s end.

The sensitive bull/bear balance tipped in favor of bears due to the strength inverse index ETFs, weakness in small-cap stocks, and semi-conductor stocks. The balance dipped below -60, but for only two days, and on Friday was approaching zero again.

The market has been very resilient, and though trading has been choppy, the declines have been well contained by the 50-day simple moving average. Moreover, as we show below, the SPY S&P-500 ETF has been trending within a narrow uptrend channel, with buying appearing at the lower trend line.

Over the past few weeks, the three strongest sectors have been utilities, health care, and consumer staples. The rest have been down until Thursday, and all of them saw a bit of bounce on Friday.

September Decline?

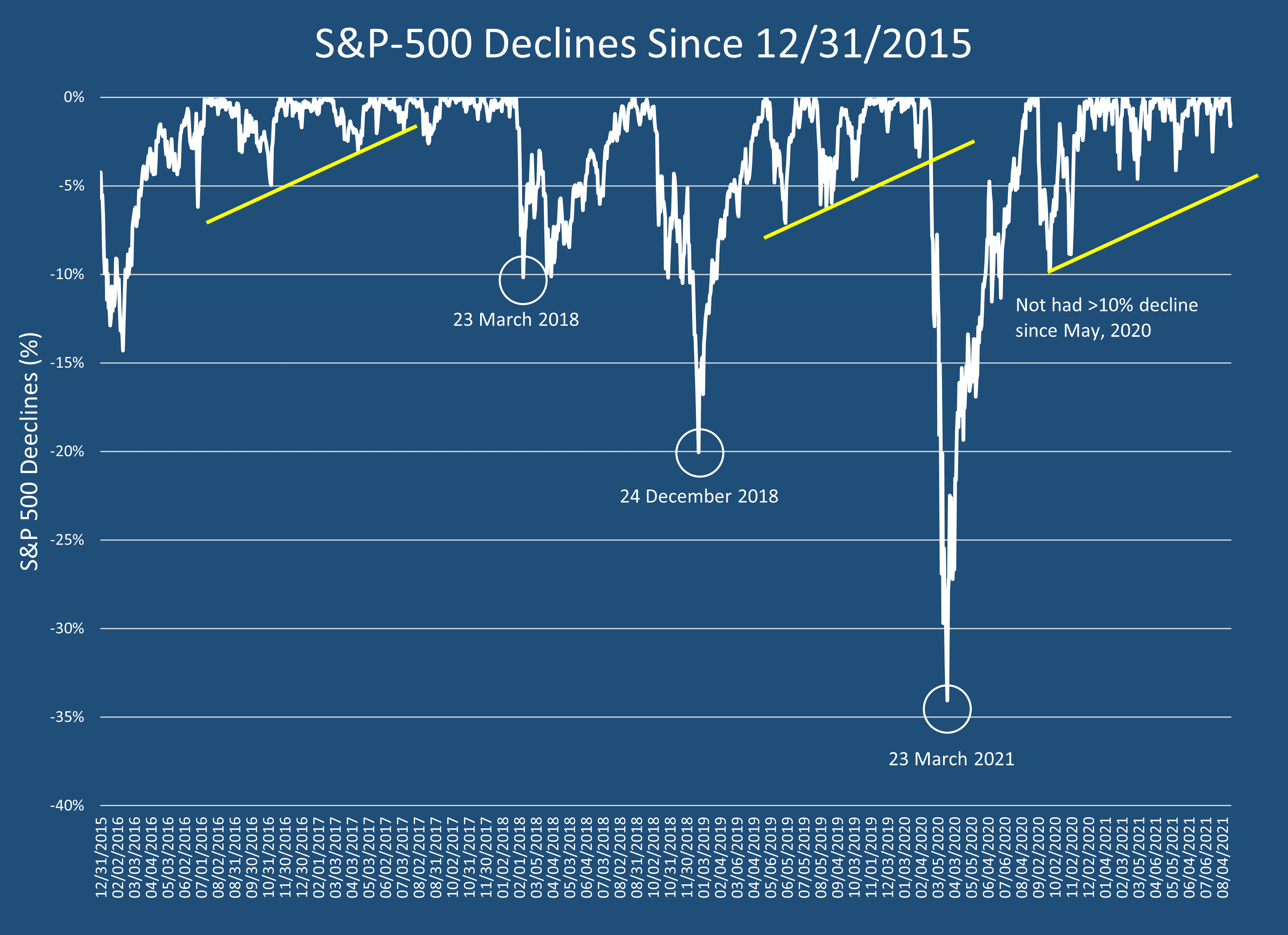

Market history shows that declines of -10% or worse happen quite frequently, about once every year and a half on average (for example, see Moss or Yardeni). Here is what declines in the S&P-500 have been since 2016 through Thursday. Note that we have not had a decline of about -10% since the middle of last year. So are we “due” for another such decline “soon”?

The market has often seen declines in September. Indeed, since 1950, the month of September has seen a drop in the S&P-500 index about 54% of the time. So, the seasonal history favors a decline next month. Indeed, the markets have already adjusted, with defensive sectors doing well over the past few weeks (see data on Vanguard ETFs below).

According to the Institute for Health Metrics, the surge in COVID-19 cases that started in the US Southeast is projected to peak soon.

Their forecast for deaths is also expected to peak a few weeks later.

The FOMC meets on September 21-22, at which time they are expected to lay out their plan to taper bond purchases. If COVID-19 cases have begun to decline, as the IHME models suggest, they may stick to a gradual tapering that will not surprise the markets. Hence, optimistically, even though there may be some precautionary selling ahead of the Fed meeting, we may not get the 10% decline many expect.

There is also the possibility of another surge in the Fall after grades K-12 return to school, colleges reopen and football season with its large crowds gets underway from high schools, colleges to the NFL. So the virus still has plenty of room to run. But, who can be sure what the virus will do?

Instead of guessing what could happen, we should keep an eye on the price channel that has contained the S&P-500 prices so far. Any serious sell-off will push prices below the lower trend line, which could be the best sign of a serious decline.

Wrap-up

If you like to do your own research, my posts should give you a good starting point, with context and suggestions. You can visit my website, chandeindicators.com, for more information and ideas. I hope you will stay tuned and help by subscribing and recommending it to your friends and colleagues.

Thank you for spending some time with me.

Disclaimer

And now for some housekeeping. This publication is for “edutainment,” education, information, and entertainment purposes only. It is not to be construed as investment advice. Past performance is not necessarily indicative of future results. Our disclaimer at chandeindicators.com is included herein by reference.