How to Exploit Rising Rates

Rising rates and a losing first week imply weak stock index returns for 2022.

Overview

The US 10-year yields ended the week near 1.77%, well above important technical resistance at 1.70 percent.

Rates rose sharply this week after the release of the minutes of the December FOMC meeting, as the market concluded monetary conditions would tighten earlier and faster.

The S&P-500 had a losing first week of trading in the new year, an occurrence that has historically foreshadowed flat-to-down full-year returns since 1950.

Tech stocks were down significantly this week, though they had a positive year last year even as rates rose gradually.

The US 10-year yield broke above a key barrier near 1.7%. Chart courtesy TradingView.com.

Key Question

Now that rates have broken through the 1.7% barrier, are there areas in the market that might benefit from rising rates? We look at stocks in the banking and energy sectors.

Performance Summary

The stock market had a losing week, primarily due to rising rates. Though the FOMC had said they would raise rates, they had not said much about how they would manage their balance sheet. So the market reacted to a new discussion on how the Fed would manage their balance sheet. The Dow 30 index, with exposure to financials and energy names, held up well, as did the equal weight RSP. The QQQ fared worst of all, as P/E multiples shrank rapidly.

The volatility of December trading returned as the S&P-500 index stalled at the 4800 level. As a result, the sensitive net bull/bear balance tilted in favor of bears at the end of the week.

As interest rates rise, financial stocks tend to do well, along with stocks tied to the energy and industrial sectors. We have plotted the short-term and long-term trend strength of key sectors in the US equity markets below. The strongest sectors are in the upper-right-hand quadrant and the weakest in the lower-left-hand quadrant. Financials (XLF, KBE, BRE), along with energy (XLE) and industrials (XLI), were strong this week.

The key to the symbols in the chart above is tabulated below.

Historical data from the Stock Trader’s Almanac suggests that as go the first five days of trading, so goes the stock market’s annual returns. Since 1950, negative returns in the first week have pointed to flat-to-down yearly market performance. Naturally, this does not guarantee that the S&P-500 index (or the SPY ETF) will automatically have a losing year. However, a broad trading range is certainly possible, and I have marked some probable support for the market in the SPY chart below.

Taking Advantage of Rising Interest Rates

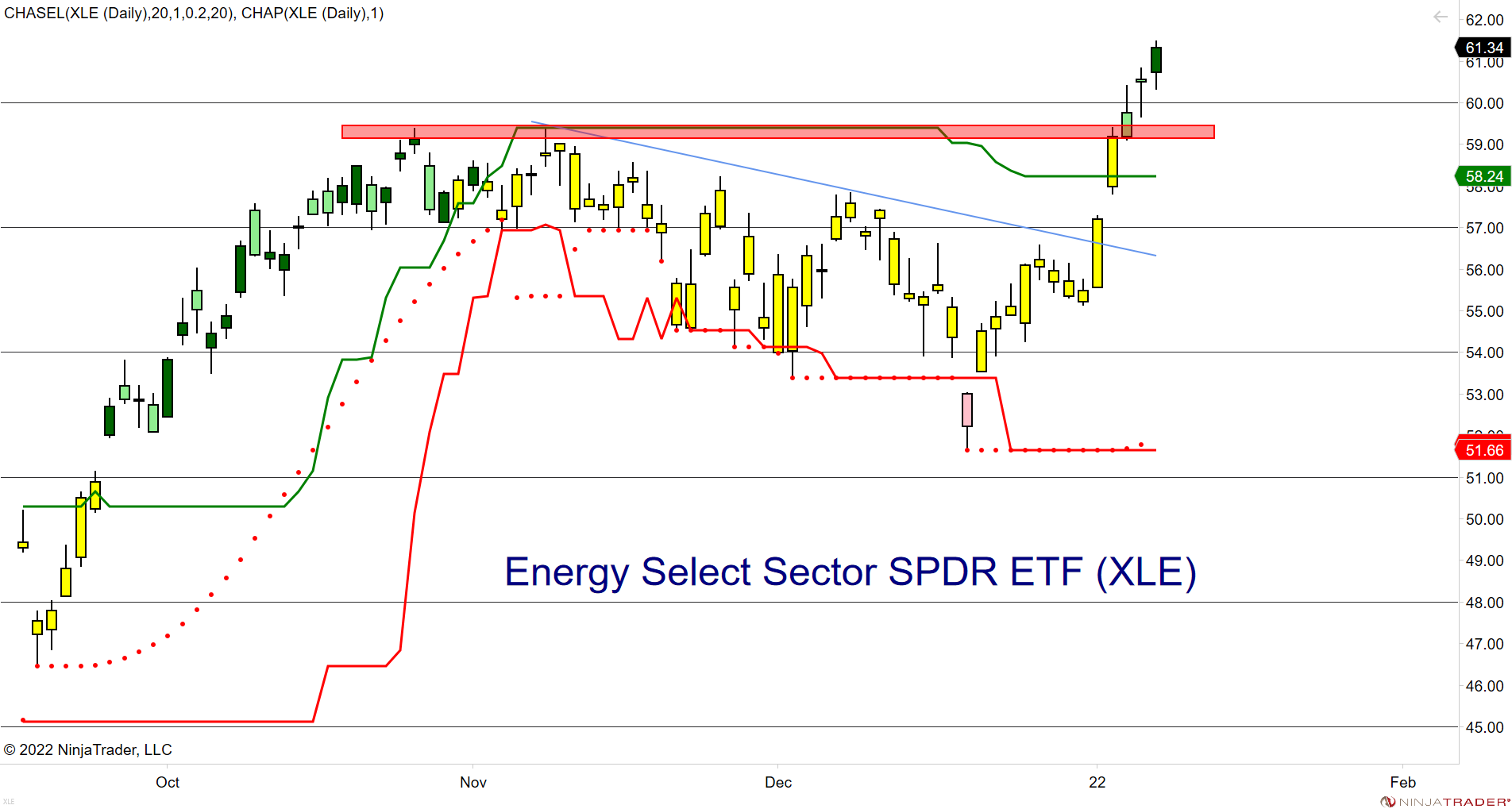

The top-level sector analysis suggests that banks, energy stocks, and industrials might benefit from rising rates. Now naturally, they will not go up in a straight line. But if your investing horizon is, say, 2~3 years, then these sectors could offer good opportunities. For example, the breakout in the energy sector (XLE) and financial sectors (XLF) should be clear from the charts below.

The Financials sector has risen above its October highs.

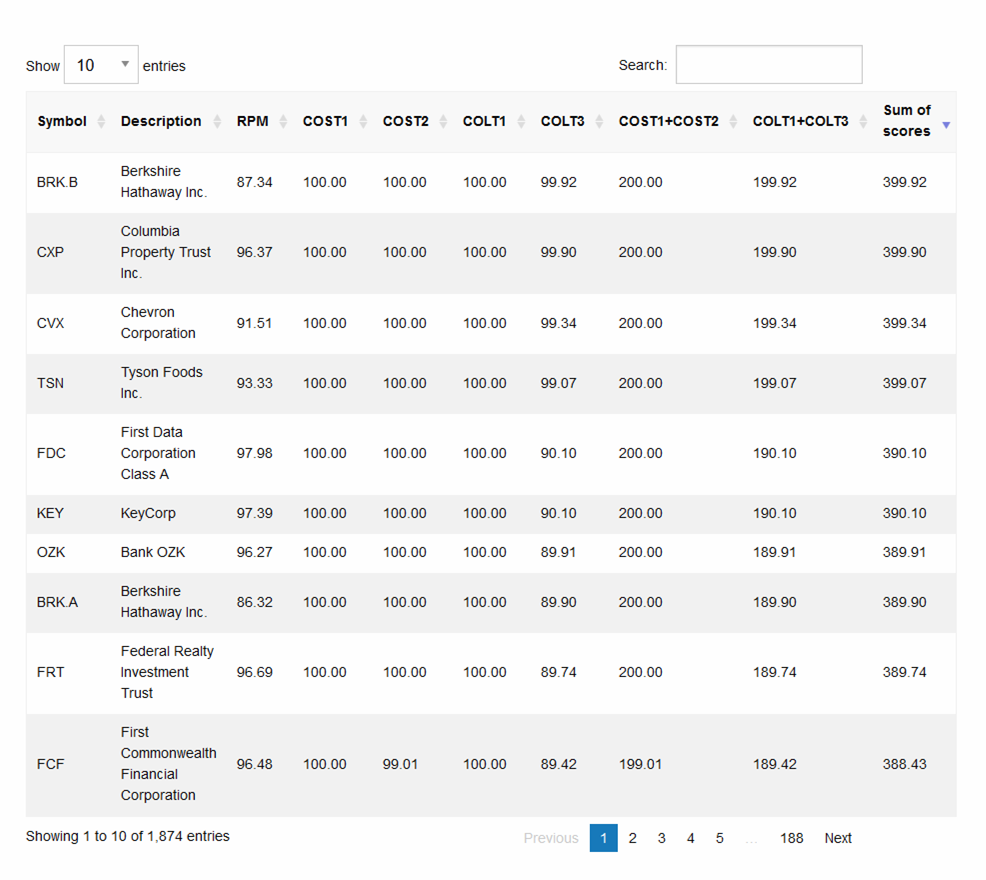

Here is a look at the StockFinder table for chandeindicators.com as of Friday. The table is sorted by the last column (Sum of scores), and the strongest stocks have a combined score near 400. Some of the leading stocks were Chevron (CVX - Energy sector), Berkshire Hathaway (BRK.B - Financials), and Key Corp (KEY - Financials). You can look through the table for more ideas.

A chart for Berkshire Hathaway below leaves no doubt about its strong response to rising interest rates.

Wrap-up

My posts should give you a good starting point, with context and suggestions if you like to do research. Then, you can visit my website, chandeindicators.com, for more information and ideas. I hope you stay tuned and help by subscribing and recommending it to your friends and colleagues.

Thank you for spending some time with me.

Disclaimer

And now for some housekeeping. This publication is for “edutainment,” education, information, and entertainment purposes only. It is not to be construed as investment advice. Past performance is not necessarily indicative of future results. Our disclaimer at chandeindicators.com is included herein by reference.