Double-Digit Gains Likely by Year-end

Double-Digit Gains Likely by Year-end

Will history repeat? We analyze monthly returns from 1950.

Overview

The economy created an estimated 372,000 payroll jobs in June, contrary to expectations.

Elsewhere, recession red flags continued to fly: the 2-10 Treasury note spread inverted, and the price of copper showed severe weakness. The NY Times has a handy summary here.

A critical CPI report is due next week (Wednesday 07/13), and the Cleveland Fed forecasts a reading of 8.67% (vs. the 8.60% previous reading). The market’s reaction will be a clue to the durability of a summer rally.

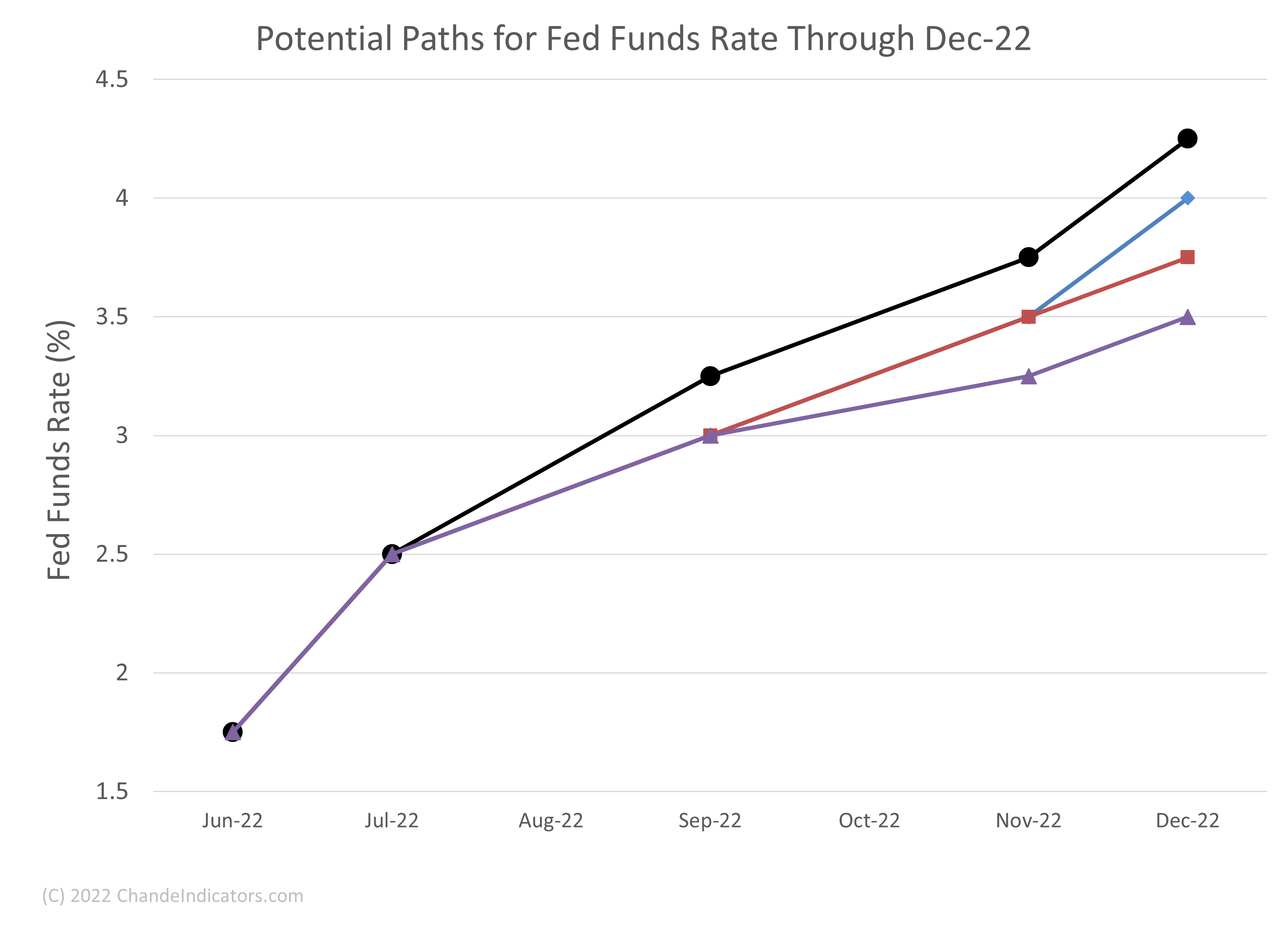

The FOMC has no reason to shrink from a 75-bp bump in the Fed Funds rate later this month. However, since the committee wants to exceed the neutral rate expeditiously, here are a few possible paths for the Fed Funds rate through year-end. The actual course will depend on incoming data.

The exact path of the Fed Funds rate is of great interest to the markets.

Key Question

What can we expect for S&P-500 returns over the next six months? To answer this question, we review the historical tendencies since 1950.

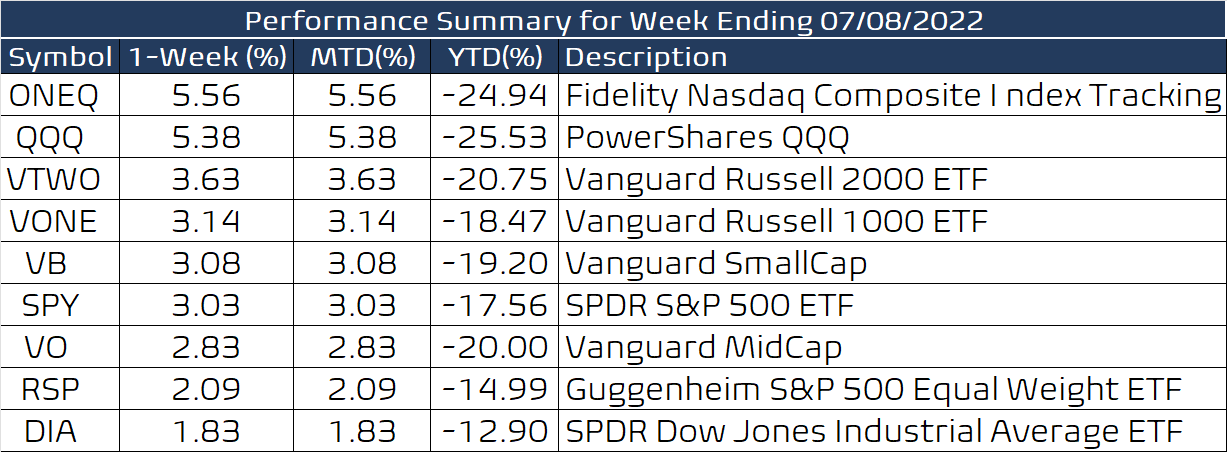

Performance Summary

A positive week for technology stocks, a possible harbinger of a trend change, particularly after withstanding today’s unemployment report. However, the CPI report is due Wednesday, so I am still cautious.

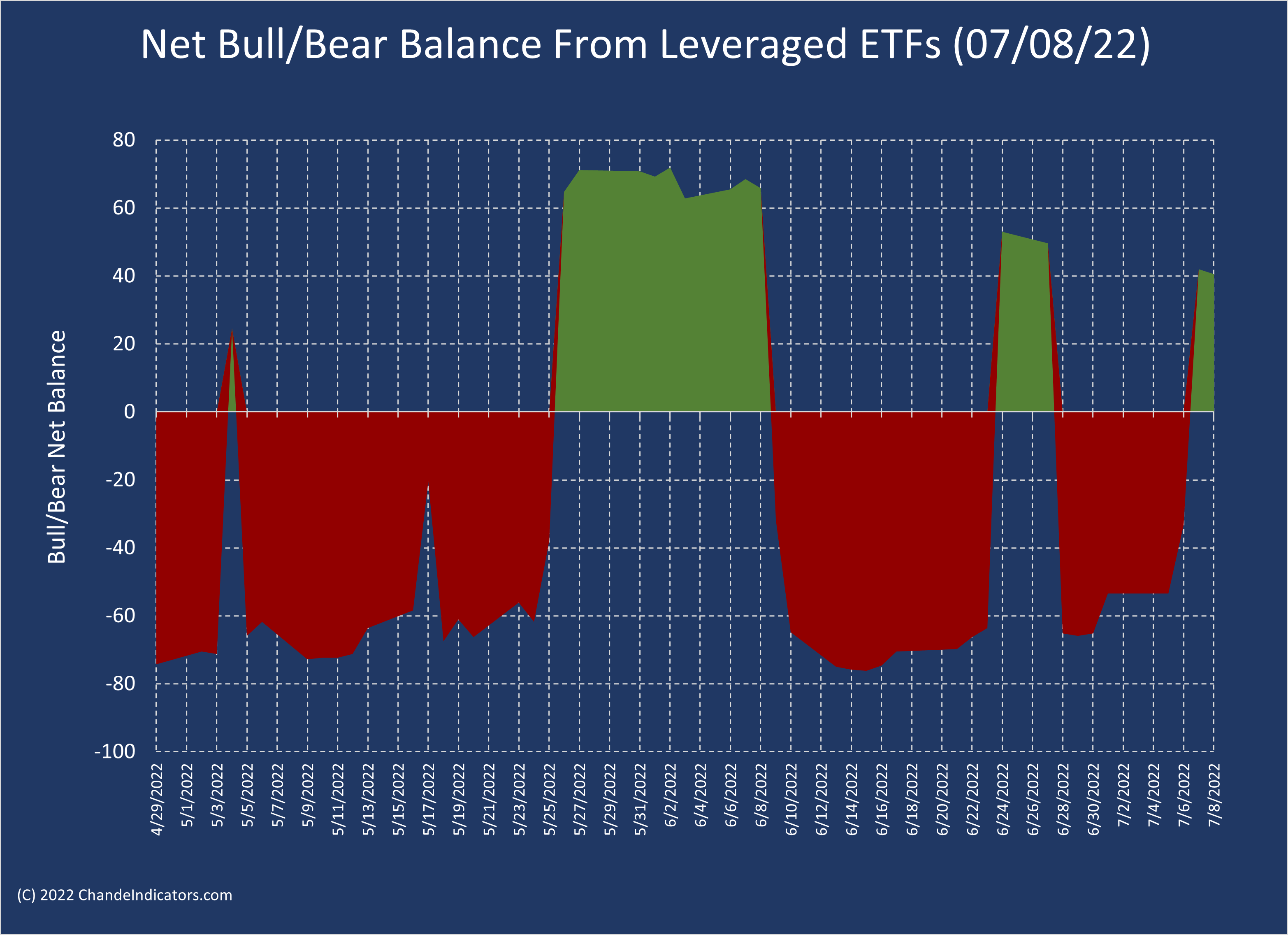

The net bull-bear balance has turned positive but is below the +60 level needed for bullish confirmation.

The S&P-500 September contract has made a higher low this week, and its short-term trend has turned up. That is also the case with the QQQ chart below. The indicator in the lower panel is a good model for the short-term trend (+100 = up, -100 = down).

Expect Positive Returns For H2

We have just lived through a rather dismal six months of relentless selling. So what can we reasonably expect over the next six months? The environment is tricky: an aggressive Fed, mid-term elections, and a resurgence of COVID-19 (via variant BA.5).

We turn to an analysis of monthly S&P-500 data since 1950. Note that my analysis of these data is context-free, i.e., I have not accounted for what traders were thinking across time. It is also important to note that the underlying technologies for analysis, trading, and information sharing have evolved exponentially, so one can reasonably question whether comparisons with 60-70 years ago markets even make sense.

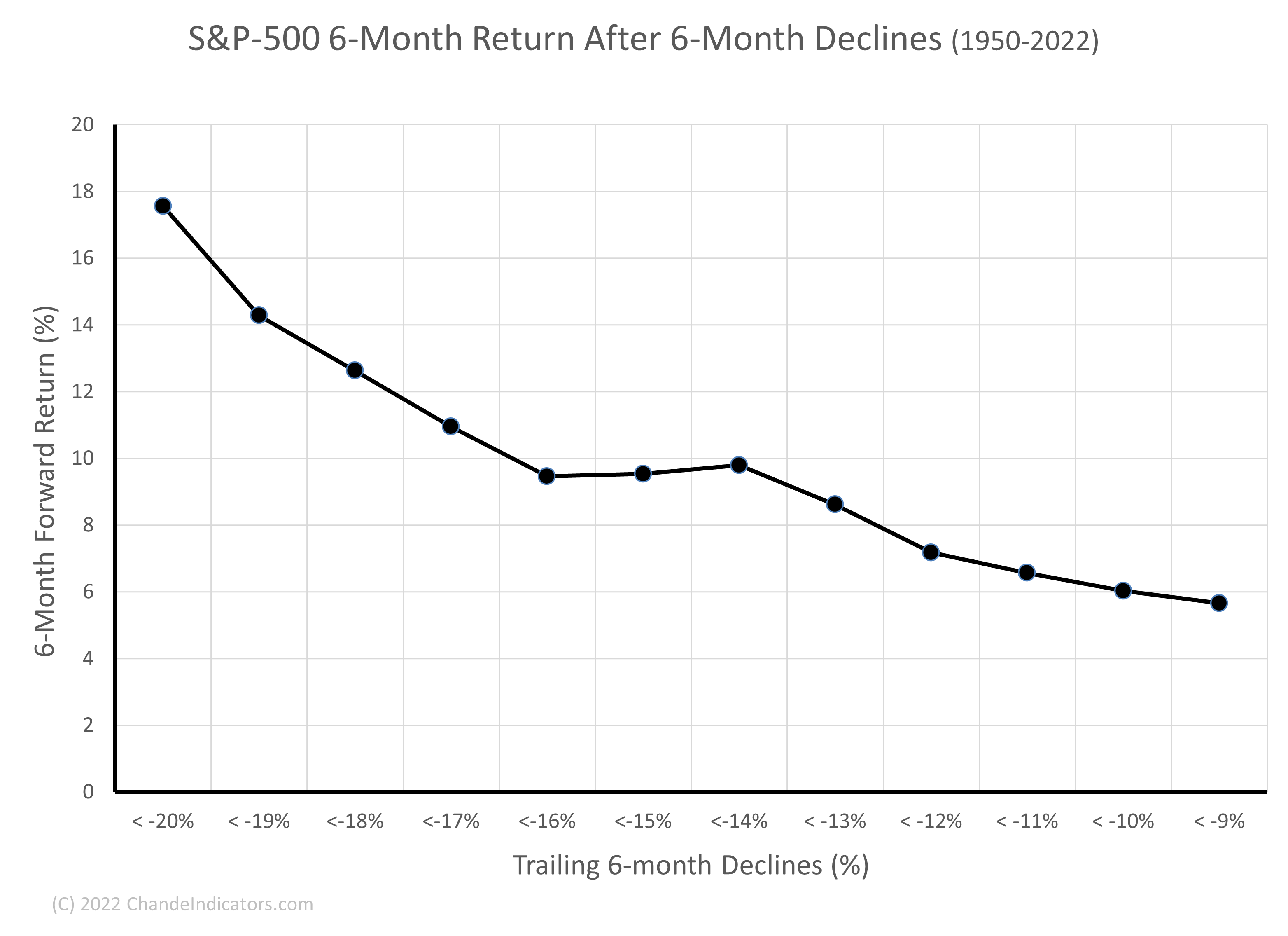

First, I calculated rolling 6-month returns and compared them to returns over the subsequent six months. Then, I zoomed in on those intervals during which the market declined by -9% or worse. In general, there is an upward bias in the data, suggesting that, on average, the market has rallied after negative six-month returns worse than -9%.

We focus on the left edge of the chart, which implies a 17.5% gain through the end of the year. Since the June S&P-500 close was approximately 3785, a +17.5% gain puts us near 4450.

I also looked at the probabilities for the above gains. The sample size is data-limited, but the likelihood of positive returns over the next six months is relatively high.

Will history repeat? Various environmental variables, such as P/E ratios and sentiment readings, have contracted sufficiently to improve the technical picture. The average of the Wall Street year-end forecasts is about 4600, with a median of 4700 and a mode of 4800. In other words, the major brokerages are more bullish than I am. Naturally, I would be delighted to be wrong.

Looking for Suggestions

I have uploaded some short videos introducing some topics in technical analysis at the request of some friends. Here is a sample. If you have a request or two, feel free to drop me a line (admin@chandeindicators.com).

Wrap-up

My posts should give you a good starting point, with context and suggestions if you like to research. Then, you can visit my website, chandeindicators.com, for more information and ideas. I hope you stay tuned and help by subscribing and recommending it to your friends and colleagues.

Thank you for spending some time with me.

Disclaimer

And now for some housekeeping. This publication is for “edutainment,” education, and entertainment, not for investment advice. Past performance is not necessarily indicative of future results. Our disclaimer at chandeindicators.com is included herein by reference.

.